First Quarter 2026: The S&P 500 Is Not A Retirement Strategy

The first quarter of 2026 reminded investors that markets do not move in a straight line. After very strong positive returns over the past 3 years, stock prices around the world pulled back, inflation picked up again, and interest rate cuts were pushed further into the future, even as the overall U.S. economy continued to grow.

The U.S. economy: slower but still growing

The U.S. economy entered 2026 growing more slowly but not in recession. Consumer and business spending remained positive, helped by job growth and wage gains, even as surveys showed many Americans still feel cautious or pessimistic about the economy. Rising energy prices, driven in part by ongoing Middle East tensions, pushed headline inflation back above 3% and led the Federal Reserve to signal that interest‑rate cuts are likely to come later and more gradually than markets had hoped. Current forecasts still call for U.S. growth around 2% this year, with inflation settling above the Fed’s 2% target for now.

Stock markets: leadership shifted under the surface

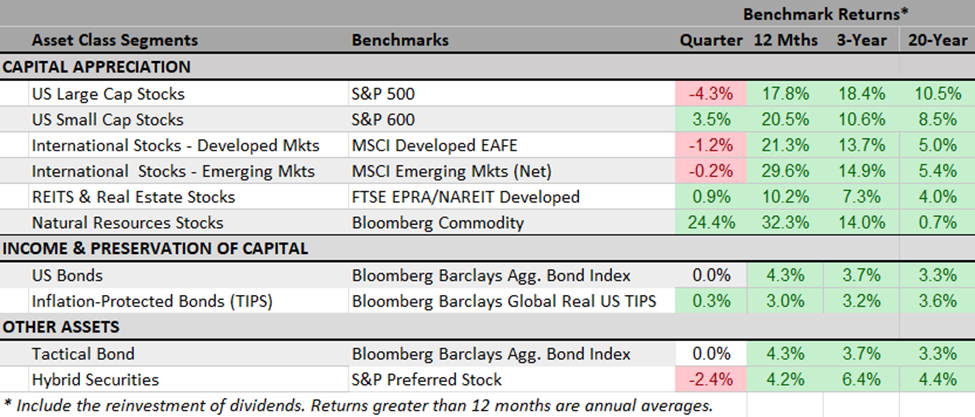

After strong gains in 2023–2025, major U.S. stock indexes declined in Q1. The S&P 500 fell roughly 4% for the quarter, and large‑cap growth and technology shares gave back some of their previous outperformance as investors worried about high valuations, higher energy costs, and delayed rate cuts.

Under the surface, however, the “average” stock outperformed the major indexes: small-cap stocks and value strategies eked out gains, indicating that the market leadership rotation away from the largest technology names, which began in Q4 2025, continued in 2026. Large growth stocks declined 13%, marking their worst quarter since the second quarter of 2022, when they lost 30%.

Stocks of companies exposed to Trump’s tariffs, such as construction firms and appliance makers, climbed after the Supreme Court struck down many of the duties in a long-awaited February ruling—even as hundreds of companies demand refunds from the U.S. government for lost profits.

Outside the U.S., results were mixed but generally somewhat better. Developed international and emerging‑market stocks posted small losses in the low single digits, helped by more moderate inflation. The war in Iran throughout March had a more negative impact overseas, as European and most Asian economies are more sensitive to energy costs.

Bonds, cash, and commodities

Bond markets came under renewed pressure as investors adjusted to the idea that interest rates may stay higher for longer. Core investment-grade U.S. bond returns were flat. Credit spreads widened somewhat, especially in Europe and emerging markets.

Short‑term cash yields remained attractive by recent historical standards, but the prospect of delayed Fed cuts also meant less price support for longer‑term bonds.

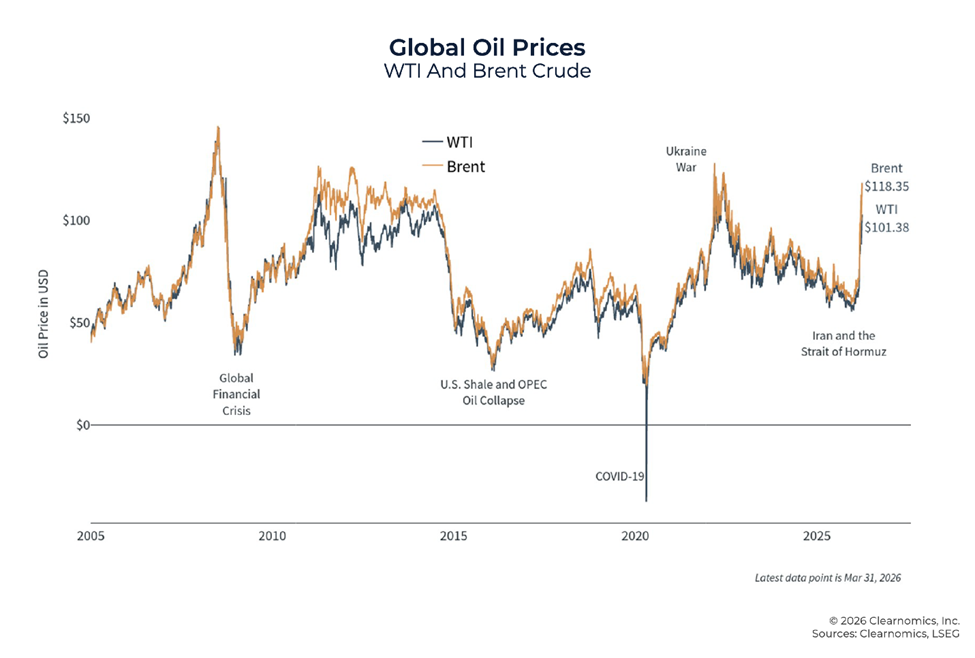

Commodities had a volatile yet strong quarter, as oil prices jumped, reinforcing their role as diversifiers when inflation and geopolitics are in the headlines. The shutdown of the Strait of Hormuz also blocked about 20% of the supply of liquefied natural gas (LNG), on which fertilizer makers in Europe and elsewhere rely.

Inflation: improving trend, renewed worries

The bigger picture is that inflation has come down sharply from its peak over the past couple of years, but the “last mile” back to central bank targets is proving bumpy. In the U.S., core inflation is now expected to run somewhat above 3% this year as higher energy prices and persistent goods and services costs keep price pressures from fully returning to 2%. Globally, inflation is expected to continue easing, with Europe and some emerging markets seeing more progress than the U.S., creating differences in how various central banks may move interest rates.

What this means for your portfolio

For long-term investors, periods like Q1 are a normal and expected part of investing. They reset expectations, cool down segments of the market that have run ahead of fundamentals, and reward diversification across companies, sizes, regions, and asset classes. Your portfolio is built with these environments in mind: a mix of stocks, bonds, cash, and other assets designed to balance growth and resilience rather than trying to predict each quarter’s headlines.

What makes the current situation unique is that the underlying fundamentals have not deteriorated as sharply as the headlines might suggest. Corporate earnings are still growing at a double-digit annual rate, well above the historical average. The labor market, while softening in payroll data, remains relatively healthy considering demographic trends.

Bond yields continue to offer meaningful income compared to the past two decades. Across asset classes, diversification has been doing its job, with energy, commodities, and international equities providing balance when U.S. large-cap stocks have struggled.

At the same time, there are genuine issues that warrant thoughtful attention. Inflation remains stubbornly above the Federal Reserve's 2% target, and energy supply-side shocks could further complicate matters. Valuations remain elevated relative to long-term history, especially in sectors that have outperformed in recent years. The AI investment cycle continues to advance, with the potential for widespread disruption across sectors. The U.S. dollar, fiscal deficits, and geopolitical tensions each carry implications that extend across asset classes and geographies.

The S&P 500 Is Not A Retirement Strategy

Over the past 15 years, investors have been well rewarded for holding the S&P 500, the primary benchmark for U.S. large-cap stocks. Its strong performance has shaped expectations, leading many to assume that recent returns will persist. As a result, we’re often asked by prospective clients: “Why diversify when I can just invest in the S&P 500?”

The challenge lies in those expectations and specifically, what investors expect the S&P 500 to deliver going forward, especially when the goal shifts to funding retirement. It’s easy to forget that the index returned nothing during the first decade of this century (2000–2009).

History shows that periods following concentrated, growth-driven rallies are often followed by more muted returns for the S&P 500 and growth-oriented investors. In contrast, portfolios built with broader diversification, attention to valuation, lower volatility, and an emphasis on quality have tended to produce more consistent, goal-oriented outcomes, regardless of which assets performed best in the prior cycle.

While these more risk-aware portfolios may not capture the full upside in strong bull markets, they can help limit downside risk during market declines. This becomes especially important for investors transitioning from saving to withdrawing assets, when consistency matters more than outperformance.

We will continue to monitor global developments and make thoughtful, incremental adjustments as needed. Most importantly, we remain focused on your long-term objectives and on maintaining a disciplined, diversified strategy designed to maximize your probability of achieving them.

Disclosure Brochure Offer

Securities laws require Bristlecone to provide clients each year with the latest version of our disclosure brochure (Form ADV Part 2A). This form includes important information about our firm, such as our services, business practices, potential conflicts of interest, a summary of our Disaster Recovery Plan, and our Privacy Policy.

The disclosure brochure can be downloaded from our website by clicking here or from the U.S. Securities and Exchange Commission's Investment Adviser Public Disclosure website by clicking here. We'll be happy to mail you a copy free of charge (call 310-806-4141 or email clientservices@bristlecone-vp.com).

You may find additional information about our firm on our website and on the Investment Adviser Public Disclosure website. Bristlecone has adopted a Code of Ethics and will provide a copy to clients upon request.

Contact us immediately if your investment objectives or financial circumstances change. Such changes could affect how we manage your portfolio and will be added to your client file. You should contact us at any time during the year if your investment goals or financial circumstances change. If your portfolio includes individual equity securities, you are responsible for voting proxies for those investments. We typically do not vote client proxies unless specifically requested.

One of Bristlecone Value Partners’ principles is to communicate frequently, openly, and honestly. We believe that our clients benefit from understanding our investment philosophy and the process behind it. Our views and opinions regarding investment prospects are "forward-looking statements" and may not be accurate over the long term. While we believe we have a reasonable basis for our appraisals and confidence in our opinions, actual results may differ materially from our expectations. Information provided in this blog should not be considered as a recommendation to purchase or sell any particular security. You can identify forward-looking statements by words like "believe," "expect," "anticipate," or similar expressions when discussing particular portfolio holdings. We cannot assure future results and achievements. You should not place undue reliance on forward-looking statements, which speak only as of the date of the blog entry. We disclaim any obligation to update or alter any forward-looking statements, whether as a result of new information, future events, or otherwise. Our comments are intended to reflect trading activity in a mature, unrestricted portfolio and might not be representative of actual activity in all portfolios. Portfolio holdings are subject to change without notice. Current and future performance may be lower or higher than the performance quoted in this blog. References to indexes and benchmarks are hypothetical illustrations of aggregate returns and do not reflect the performance of any actual investment. Investors cannot invest directly in an index, and returns do not account for the deduction of advisory fees or other trading expenses. There can be no assurance that current investments will be profitable. Actual realized returns will depend on, among other factors, the value of assets and market conditions at the time of disposition, any related transaction costs, and the timing of the purchase. Economic factors, market conditions, and investment strategies will affect the performance of any portfolio, and there can be no assurance that a portfolio will match or outperform any particular index or benchmark. Past Performance is not indicative of future results. All investment strategies carry the potential for profit or loss. Changes in investment strategies, contributions, or withdrawals can materially alter a portfolio's performance and results. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment will be suitable or profitable for a client's investment portfolio. This content is developed from sources believed to provide accurate information, and it may not be used to avoid any federal tax penalties. Please consult legal or tax professionals for specific information regarding your individual situation. The opinions expressed and material provided are for general information and should not be considered a solicitation for the purchase or sale of any security.